Goodrich Petroleum Report - A Look

Goodrich Petroleum gave a 4th Quarter and Annual Presentation on February 27, 2015.

Here we will take a look at selected slides and provide a little commentary to give our impressions and understanding of the information presented.

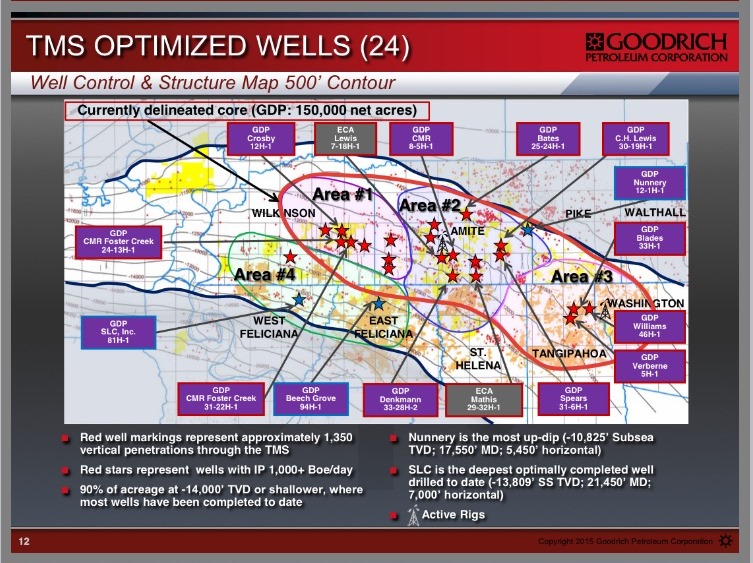

First is the latest TMS delineated core map as outlined in red with 4 areas in and around the delineated core.

The "Core" of the Core appears to be Area 2.

That said, Area 3 is the current hot area in that Goodrich is focusing efforts there, likely in part due to the 1/3 partnership with Sinnopec.

Goodrich management indicated that Area 4 and delineation wells in other areas have shown promise with a slower decline rate indicated.

In other words, none of these areas should be considered, just year, as better or worse than the others insofar as potential goes.

........................

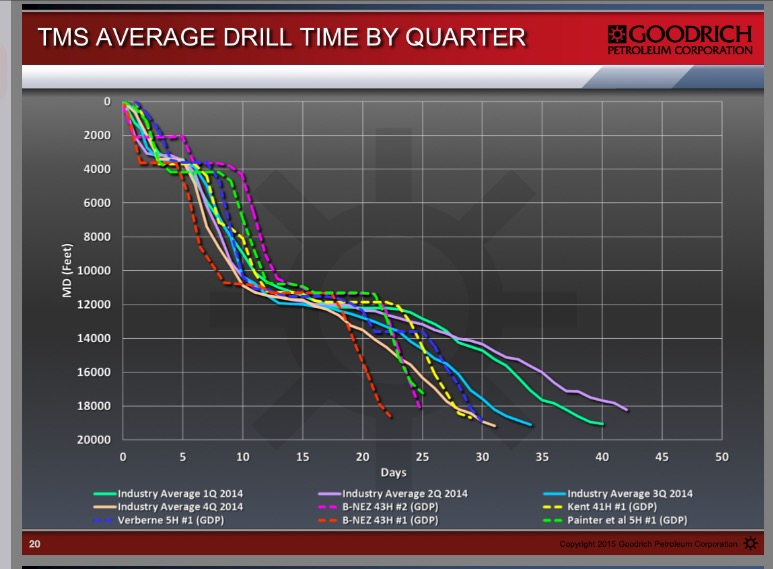

The Average Drill Time by Quarter slide as shown below is very interesting.

Specifically, the time in the 2nd quarter of 2014 actually increased over 1st quarter times.

I attribute this to the learning curves of Halcon and Sanchez.

Then, in the in the 3rd quarter things began to click and times dropped significantly and continued to drop in the 4th quarter.

It would appear, based on drilling times so far, the 1st quarter of 2015 will see a continued reduction in the average time to drill a well.

.......................................

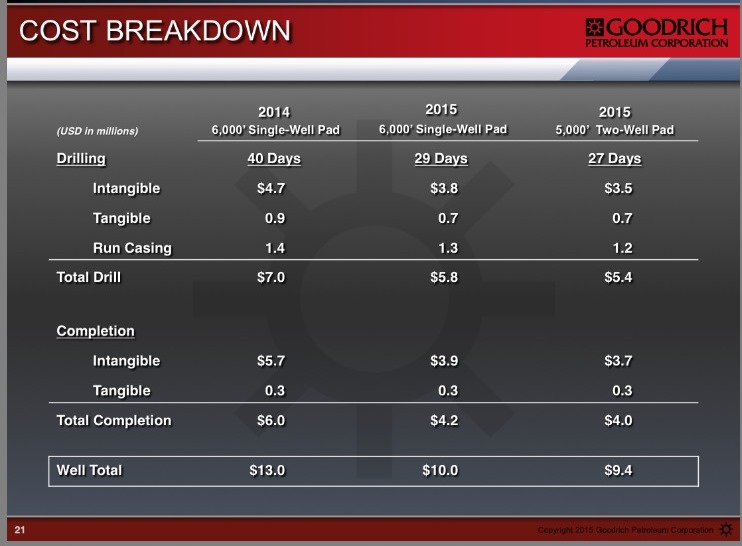

The drop in drilling times, along with previously announced improvements by Goodrich in the costs of fracking and then combined with multi-well drilling have caused a reduction in the total cost to bring a well into production.

The Cost Breakdown below for 6,000 foot horizontal single wells in 2014 and 2015 and 5,000 foot multi-well costs in 2015 are shown in the slide below.

Frankly, costs early in 2014 were likely closer to $15 million per well rather than the $13 million per well shown above.

Lower service prices were also mentioned as a factor in the lower completed well costs shown. Lower charges, faster drilling times, more economical fracking designs and multi-well drilling have all combined to bring the cost for a completed TMS well to the $9.4 million level and it is anticipated that these costs will continue to drop.

Even without continued improvements, at these current cost levels a return to the TMS seems very promising.

............................

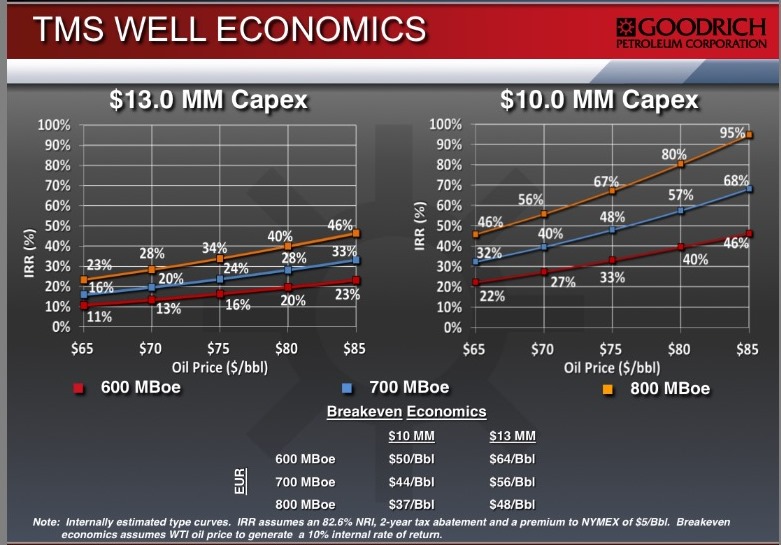

Goodrich gave us a picture of the percentage profits possible from these wells at various price levels, using various assumptions (severance tax, royalty payments, internal rates of return, and varying estimated ultimate recoveries).

Though not shown, at $100 a barrel, TMS wells will more than double the money invested.

And, after all, that's why these companies are here...to make a profit.

.................

There is a saying, "Figures Lie and Liars Figure."

It is only natural to question these rates of return.

But, personally, these numbers make sense to me.

The main question that I have is whether the estimated ultimate recovery numbers are reasonable.

And, I suspect the question on these recovery numbers is the only reason that EnCana isn't focused on the TMS rather than spreading itself out to the Permian Basin and the Eagle Ford.

Goodrich seems convinced the EUR's are reasonable, but the evidence needs to be more concrete to convince a joint venture partner to jump in with them and fully develop its holdings in the TMS.

So, 2015 becomes the year we wait for prices to improve while production curves are more firmly established.

Assuming both occur, we very well may see 2016 become the year full development of the TMS begins.

Stay Tuned!